All Categories

Featured

Table of Contents

Another type of advantage debts your account balance regularly (yearly, for example) by setting a "high-water mark." A high-water mark is the highest possible value that an investment fund or account has reached. The insurer pays a fatality benefit that's the greater of the present account value or the last high-water mark.

Some annuities take your preliminary investment and instantly include a certain portion to that quantity every year (3 percent, for example) as a quantity that would certainly be paid as a fatality benefit. Guaranteed return annuities. Beneficiaries then receive either the real account value or the preliminary investment with the annual rise, whichever is better

You can pick an annuity that pays out for 10 years, but if you pass away prior to the 10 years is up, the staying settlements are guaranteed to the recipient. An annuity fatality benefit can be practical in some scenarios. Below are a couple of examples: By helping to avoid the probate process, your recipients might receive funds quickly and easily, and the transfer is exclusive.

Tax-efficient Annuities

You can generally pick from numerous choices, and it's worth checking out all of the options. Choose an annuity that works in the manner in which finest helps you and your household.

An annuity helps you collect cash for future income needs. The most ideal use for revenue repayments from an annuity contract is to fund your retired life.

This product is for educational or instructional functions only and is not fiduciary financial investment recommendations, or a protections, investment technique, or insurance product suggestion. This product does rule out an individual's own purposes or situations which must be the basis of any financial investment choice (Fixed-term annuities). Financial investment items may undergo market and various other threat elements

How does an Annuity Withdrawal Options help with retirement planning?

All warranties are based on TIAA's claims-paying capability. Income protection annuities. TIAA Standard is a guaranteed insurance agreement and not a financial investment for government safeties legislation purposes. Retired life settlements refers to the annuity earnings obtained in retirement. Guarantees of dealt with regular monthly payments are only related to TIAA's repaired annuities. TIAA might share revenues with TIAA Conventional Annuity proprietors via declared extra quantities of interest during accumulation, higher first annuity earnings, and via more increases in annuity earnings advantages during retired life.

TIAA might supply a Commitment Incentive that is just readily available when choosing lifetime revenue. Annuity contracts might consist of terms for keeping them in pressure. TIAA Typical is a fixed annuity product provided through these contracts by Teachers Insurance coverage and Annuity Organization of America (TIAA), 730 Third Avenue, New York, NY, 10017: Form series including however not restricted to: 1000.24; G-1000.4; IGRS-01-84-ACC; IGRSP-01-84-ACC; 6008.8.

Converting some or every one of your savings to earnings advantages (described as "annuitization") is a long-term choice. When earnings advantage payments have begun, you are not able to alter to another choice. A variable annuity is an insurance policy agreement and consists of underlying financial investments whose worth is linked to market efficiency.

Annuity Payout Options

When you retire, you can choose to obtain revenue permanently and/or other earnings options. The property sector goes through different dangers including changes in underlying property values, costs and revenue, and prospective environmental obligations. As a whole, the value of the TIAA Realty Account will change based on the hidden value of the straight realty, actual estate-related financial investments, actual estate-related protections and liquid, set income investments in which it invests.

For an extra complete discussion of these and various other risks, please seek advice from the prospectus. Liable investing incorporates Environmental Social Administration (ESG) factors that may impact exposure to companies, sectors, sectors, restricting the kind and number of investment opportunities available, which might result in excluding investments that do well. There is no assurance that a diversified profile will certainly boost general returns or outmatch a non-diversified portfolio.

You can not spend straight in any type of index - Annuities. Other payment options are available.

There are no charges or costs to start or quit this attribute. It's important to keep in mind that your annuity's equilibrium will certainly be lowered by the income settlements you obtain, independent of the annuity's performance. Income Test Drive earnings repayments are based upon the annuitization of the amount in the account, duration (minimum of ten years), and other aspects selected by the individual.

Flexible Premium Annuities

Annuitization is irreversible. Any kind of guarantees under annuities released by TIAA go through TIAA's claims-paying capacity. Interest in excess of the guaranteed quantity is not guaranteed for durations apart from the periods for which it is declared. Transforming some or every one of your financial savings to earnings benefits (referred to as "annuitization") is a permanent decision.

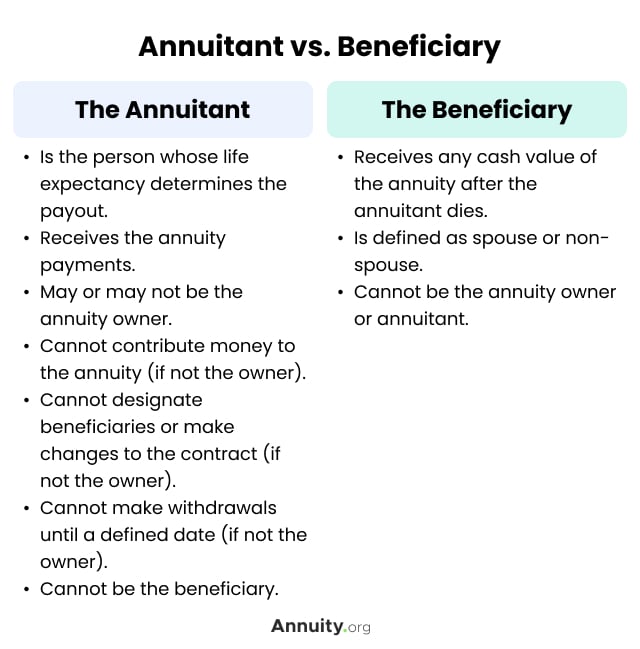

You will certainly have the alternative to name several recipients and a contingent recipient (a person marked to get the money if the key beneficiary passes away prior to you). If you don't name a recipient, the collected possessions might be given up to a banks upon your fatality. It is very important to be knowledgeable about any kind of economic repercussions your beneficiary might deal with by acquiring your annuity.

As an example, your partner could have the alternative to change the annuity contract to their name and become the new annuitant (referred to as a spousal continuation). Non-spouse recipients can not continue the annuity; they can only access the designated funds. Minors can't access an inherited annuity up until they turn 18. Annuity proceeds could leave out someone from getting federal government benefits - Annuity income.

What is included in an Senior Annuities contract?

For the most part, upon death of the annuitant, annuity funds pass to a properly called recipient without the delays and prices of probate. Annuities can pay survivor benefit numerous various means, relying on regards to the agreement and when the death of the annuitant occurs. The choice selected influences how tax obligations schedule.

Assessing and upgrading your selection can assist guarantee your wishes are executed after you pass. Choosing an annuity recipient can be as complicated as picking an annuity in the initial place. You do not require to make these complex decisions alone. When you speak to a Bankers Life insurance policy representative, Financial Representative, or Investment Expert Representative that supplies a fiduciary requirement of treatment, you can feel confident that your decisions will certainly assist you develop a strategy that offers safety and security and assurance.

{kind=link}

Table of Contents

Latest Posts

Exploring Choosing Between Fixed Annuity And Variable Annuity A Comprehensive Guide to Investment Choices What Is Fixed Indexed Annuity Vs Market-variable Annuity? Pros and Cons of Fixed Indexed Annui

Highlighting Fixed Annuity Vs Variable Annuity A Closer Look at Retirement Income Fixed Vs Variable Annuity What Is Pros And Cons Of Fixed Annuity And Variable Annuity? Benefits of Fixed Annuity Or Va

Exploring the Basics of Retirement Options A Closer Look at How Retirement Planning Works Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Fixed Index Annuity Vs Variable A

More

Latest Posts